Running Head: Exploring the Impact of Financial Toxicity in COPD

Funding Support: This work was supported by the National Heart, Lung, and Blood Institute (NHLBI) of the National Institutes of Health. SGM was supported by NHLBI award numbers F32HL176086 and T32HL007534. The Medication Adherence Research in COPD (MARC) study was supported by NHLBI award number R01HL128620. The content is solely the responsibility of the authors and does not represent the official views of the National Institutes of Health.

Date of Acceptance: March 9, 2026 | Published Online Date: March 30, 2026

Abbreviations: COPD=chronic obstructive pulmonary disease; COREQ=Consolidated criteria for Reporting Qualitative research; COST=COmprehensive Score for financial Toxicity; COST-FACIT=COmprehensive Score for financial Toxicity - Functional Assessment of Chronic Illness Therapy; FSA=flexible spending account; HSA=health savings account; IQR=interquartile range; MARC=Medication Adherence Research in COPD; OOP=out of pocket; SES=socioeconomic status; VA=Veterans Affairs

Citation: Mallya SG, Holloway K, Eaton CK, et al. Exploring the impact of financial toxicity in COPD: a qualitative study. Chronic Obstr Pulm Dis. 2026; 13(3): 216-226. doi: http://doi.org/10.15326/jcopdf.2025.0712

Online Supplemental Material: Read Online Supplemental Material (192KB)

Note: A version of these results was previously presented at the American Thoracic International Conference in San Francisco, CA on May 20, 2025 as an abstract.

Introduction

Individuals with chronic obstructive pulmonary disease (COPD), a leading cause of disability in the United States, face unique material burdens.1,2 Inhaled bronchodilators, the mainstay treatment for COPD, remain costly in the United States due to limited generic options and are estimated to contribute to almost two-thirds of out-of-pocket COPD-specific expenses across all payors.3-5 Acute exacerbations of COPD can lead to unexpected emergency department visits and hospitalizations.6 Comorbid conditions in COPD are common and can impact clinical outcomes and health care utilization.7 In addition, prevalence of COPD is disproportionately higher in individuals of lower socioeconomic status (SES), attributed to higher rates of tobacco use as well as increased exposure to environmental and occupational risks.8-10 While individuals with COPD may face high material burden, it is unknown how they manage the increased cost and its impact on their well-being.

Financial toxicity, which describes the objective material burden and subjective distress resulting from both direct and indirect costs of illness, has largely been studied in oncology, where cancer-related treatment has been associated with delaying or foregoing care, medication nonadherence, and reduced health-related quality of life.11-13 Compared with cancer-related treatment, which often involves high costs with initial diagnosis and active treatment phases, COPD care generally involves lower per-treatment costs but sustained expenditures, often accumulating later in life when individuals have a fixed income due to disability or retirement. Research on financial toxicity in COPD is limited but suggests it is common, with one study demonstrating that over half of privately insured individuals with self-reported COPD worried about medical costs.14 We previously demonstrated that difficulty affording medications was associated with worse respiratory morbidity, psychological well-being, and objectively-measured medication adherence.15 What remains unknown is the impact of financial toxicity on quality of life in COPD.

The goal of this qualitative study is to describe experiences of COPD-related financial toxicity. Specifically, we sought to characterize the sources of material burden for people with COPD, the perceived impact of this burden on self-management and well-being, and individual strategies to manage these burdens that may guide future interventions addressing financial toxicity in this population.

Study Design and Methods

Participants

A subsample of individuals enrolled in the Medication Adherence Research in COPD (MARC) study who gave permission to be contacted for future research were contacted to participate in semistructured interviews. The MARC study was a prospective multicenter cohort study between Johns Hopkins Medicine (Baltimore and Hagerstown, Maryland) and Christiana Care (Wilmington and Newark, Delaware) from 2017 through 2023. Inclusion criteria in the current study were the same as in the MARC study (age 40 years old, physician-diagnosed COPD of at least moderate severity based upon prescription of a long-term controller medication). Participants who gave permission to be contacted for future research were purposively selected for diversity in race, income, education, insurance status, and a previous survey response to a question about delaying medication refills due to cost. Interested individuals were scheduled for an interview.

All study procedures, including the need for verbal consent and consent script, were approved by the Johns Hopkins Medicine Institutional Review Board (IRB00424551). Verbal consent was obtained prior to initiation of study procedures, including audio recording of interviews. Participants were reimbursed $25 for their time.

Interviews

All interviews were conducted between August 2024 and March 2025 using a semistructured interview guide, detailed in e-Appendix 1 in the online supplement. Following a literature review, the interview guide was drafted by SGM and discussed and revised with the help of experts in behavior and qualitative research (MNE, KAR). Interviews were intended to explore sources of COPD-related material burden, mechanisms of financial distress, behavioral changes to financial or disease self-management, and interactions with health care providers.16 The guide included optional follow-up questions based on individual responses. Ongoing review of interview transcripts allowed iterative modification of questions for subsequent interviews to explore themes as they emerged.

Interviews were conducted by a female pulmonary and critical care medicine fellow (SGM) via telephone calls that were audio recorded. Recordings were transcribed by a Health Insurance Portability and Accountability Act-compliant transcription service.

Following the interview, participants completed a demographic questionnaire and the COmprehensive Score for financial Toxicity - Functional Assessment of Chronic Illness Therapy (COST-FACIT), an 11-item measure assessing financial toxicity in the prior 7 days. Respondents ranked each statement on a 5-point Likert scale. The scale has a possible range of scores from 0 to 44, with lower scores corresponding to greater financial toxicity.17 Based upon the COST-FACIT developer’s grading system, a score of ≤ 25 corresponds to at least mild financial toxicity.18

Analysis

Transcripts were analyzed using thematic analysis to provide a descriptive understanding of the impact of financial toxicity on participants.19,20 Following the completion of 10 interviews, transcripts were examined by SGM and MNE for identification of themes used to develop a codebook that was then reviewed by all co-authors. Emerging themes from subsequent interviews were iteratively added to the codebook as needed. Transcripts were coded with NVivo 13 (QSR International Pty Ltd; Doncaster, Australia) by 2 independent coders (SGM and KH). Discrepancies were addressed by the senior qualitative investigator (MNE). Coding comparison between SGM and KH was calculated using percentage agreement and Cohen’s kappa coefficient. During analysis, thematic saturation was defined as no new themes emerging for at least 3 interviews.21 A summary of findings and transcripts were presented to our patient advisory board as a form of member checking. Study reporting follows the Consolidated Criteria for Reporting Qualitative Research (COREQ).22

Results

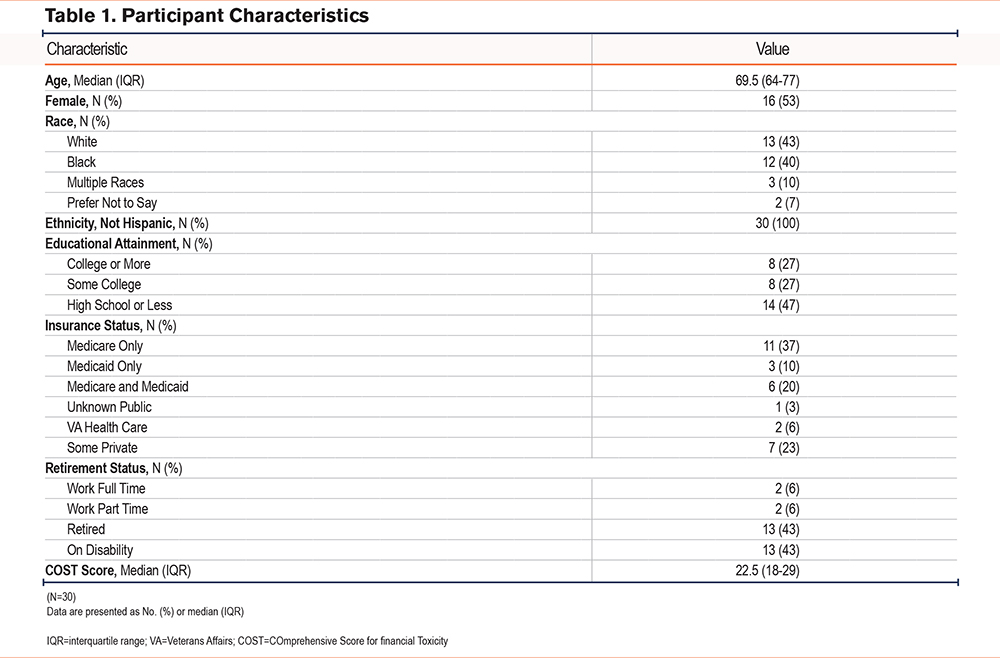

Of the 189 MARC participants who provided consent to be contacted, 63 were sent a letter describing the study before attempted contact by telephone. Of the 63, 8 had passed away, 21 were not reached despite multiple attempts, and 4 declined to participate. Thirty individuals completed interviews. Demographic characteristics of participants are described in Table 1. Of the participants, 53% were female, 43% were non-Hispanic White, 40% were non-Hispanic Black, and 10% were multiracial, with a mean age of 69.5 years. A total of 27% had a college degree or higher. The majority of participants (70%) were on public insurance only, with 37% overall on Medicare only, 20% on dual Medicare and Medicaid, and 10% on Medicaid only. Most participants were either retired (43%) or on disability (43%). The median COST-FACIT score was 22.5 (interquartile range, 18-29; mean ± standard deviation, 24.43 ± 8.05) with 63% meeting criteria18 for at least mild financial toxicity (total score ≤ 25).

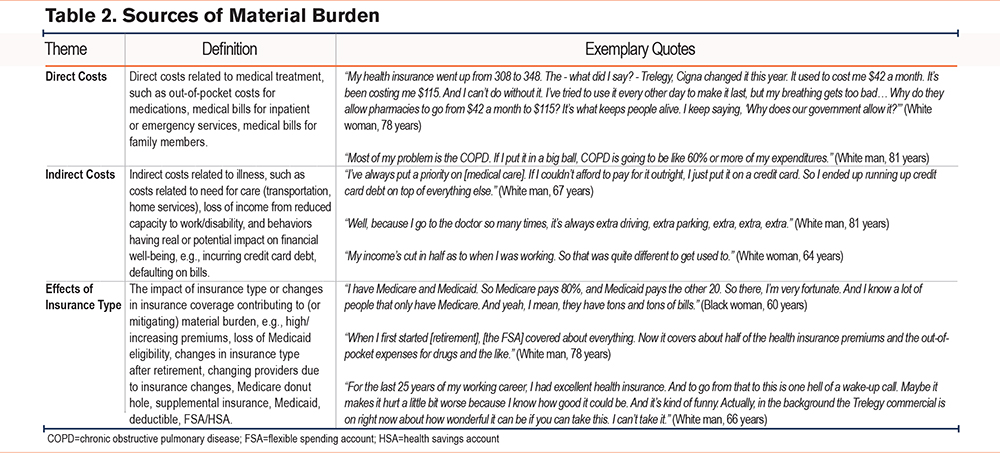

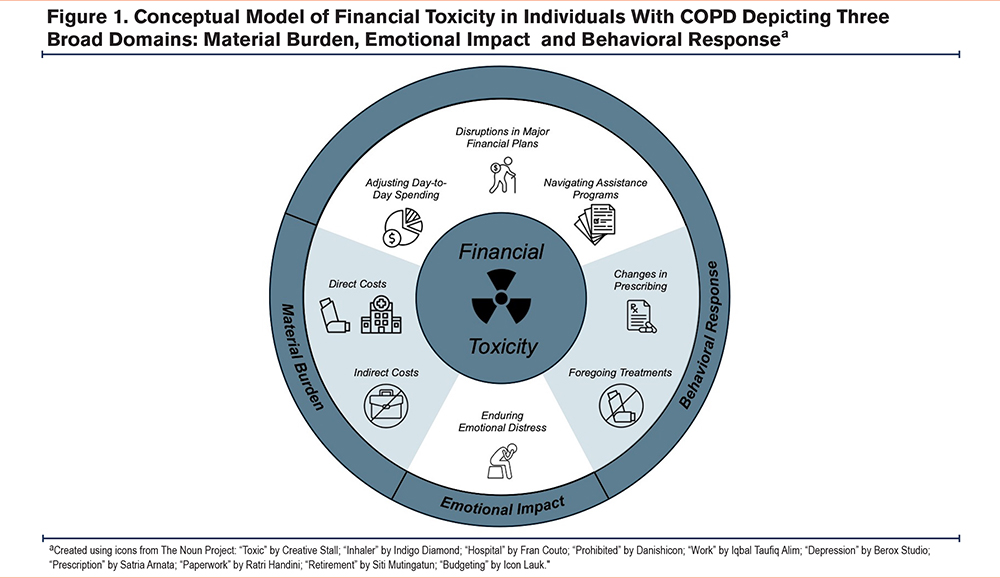

Interrater reliability of assigned interview codes was high (Cohen’s kappa = 0.84; percentage agreement 98.7%). Participants expressed a range of experiences and challenges related to the costs of medical care for COPD. Key themes that emerged were (1) the material burden of COPD, (2) adjustments to disease management, (3) adjustments to financial planning, (4) the emotional impact, and (5) communication with health care providers (Tables 2, 3, 4, and 5). A conceptual model of key themes is illustrated in Figure 1.

Sources of Material Burden

Participants described direct and indirect costs related to COPD (Table 2). Many described substantial out-of-pocket costs for inhalers, particularly those with Medicare Part D who surpassed the annual prescription drug coverage limit and entered the next coverage phase, often referred to as the “donut hole,” where the beneficiary is responsible for a greater percentage of total prescription costs. Notably, the provision of the Inflation Reduction Act23 capping out-of-pocket expenses at $2000 for Medicare Part D beneficiaries went into effect in January 2025. Some beneficiaries interviewed in 2025 who had not previously entered the “donut hole” experienced unexpected increases in out-of-pocket costs compared to the previous year due to increased cost-sharing and higher upfront deductibles. Other contributors to direct costs were medical bills from hospitalizations and increasing health insurance premiums.

“Well, I put out a fair amount of money for medications, even with Medicare Part D. The Trelegy that I take, when I end up in the ‘donut hole’ it becomes pretty significant... I'm probably out-of-pocket, probably put $3000 into various medications.” (White, man, 77)

“Up until the first of this year, [my COPD] was fairly well controlled with medication that I had been on for quite some time. My out-of-pocket cost [had been] about $90 for a 3-month supply. When I went to buy it, I found that it was $894... I never reached the ‘donut hole’ before. My medications were covered. Apparently they moved the ‘donut hole’ from the center to the beginning so that I would have to make the deductible before the medication would be paid for... So I simply stopped taking it because I couldn’t afford it.” (White, man, 66)

“It was this monstrous bill. I took the bill and I gave it to the Veterans Association (VA), and the VA could only pay as much as they were authorized. And there was a remainder of about $2000. I really stressed over that for a few months.” (Black, man, 73)

Indirect costs incurred by participants included loss of employment or early retirement resulting in lost income. Others mentioned expenses related to receiving medical care, such as transportation to and from appointments. Some individuals also described downstream effects of illness on financial well-being, such as a decline in credit score resulting from defaulting on bill payments or accumulating credit card debt.

“I live in a rural area, and my doctors are 20, 30 miles away. When I was on Medicaid, I could use the transportation from the health department, but they do not do that for Medicare... So I have to pay people to take me to the doctor, to sit there and wait on me, and bring me back.” (Black, man, 66)

“It caused me to basically get bad credit, have a lot of bills go into default.” (Black, woman, 52)

Notably, material burden varied by insurance type. Many individuals enrolled only in Medicare described higher out-of-pocket costs, particularly for inhalers, and entering the “donut hole” before the end of the coverage year. In contrast, those who had Medicaid, both Medicare and Medicaid, coverage through Veterans Affairs, or private supplemental insurance generally reported minimal out-of-pocket costs.

“I lost my [Medicaid] last year. So I'm on Medicare only, and I have to pay monthly for my health insurance. Before, I didn't have to. So for the last year, I've been paying for my health insurance. And my copays have increased, and my prescription costs have increased.” (Black, woman, 68)

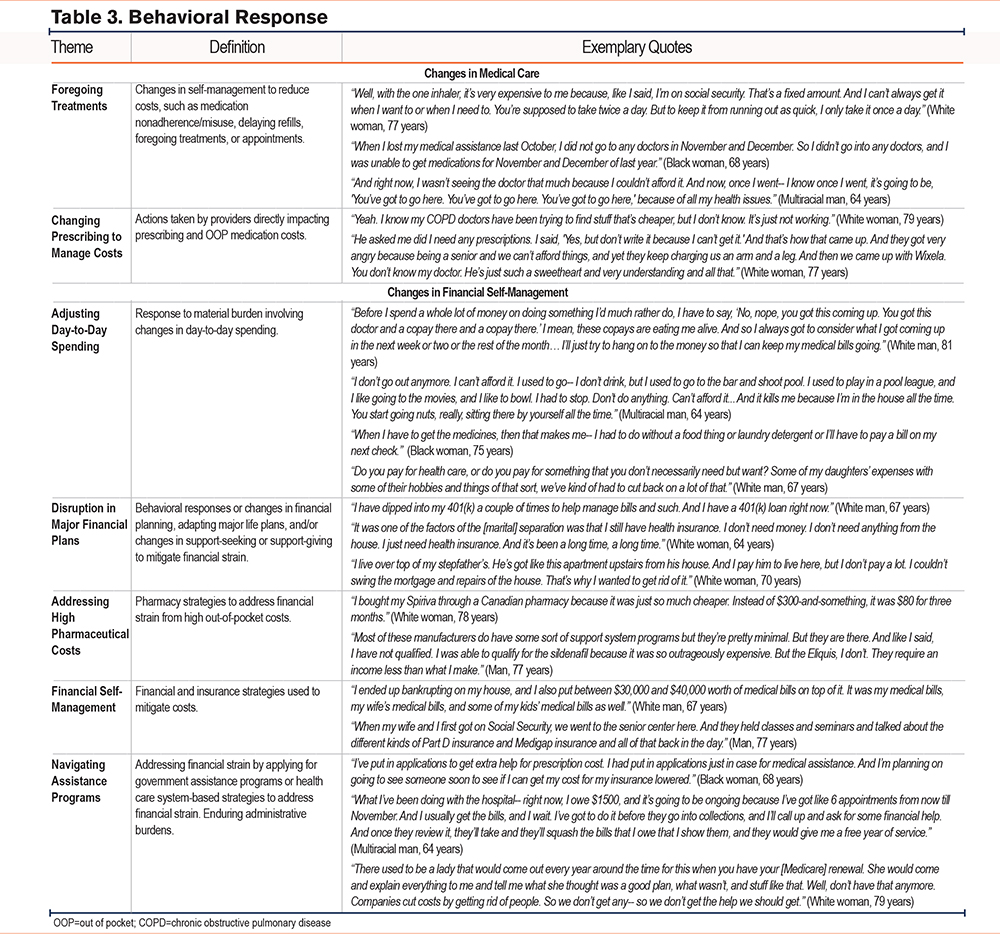

Behavioral Response: Changes in Medical Care

Participants described specific ways that costs incurred from COPD treatment impacted self-management of their disease including medication nonadherence or misuse and foregoing doctor’s visits or treatments (Table 3). Some worked with their providers to find less expensive alternatives.

“Last year when we went into the ‘donut hole,’ I stopped taking Breo [Ellipta] until we were out of the ‘donut hole.’” (White, woman, 70)

“A month ago, we found a less expensive alternative. I sold some personal assets so that I can start treating it again. The product isn't quite as effective... but it's better than nothing.” (White, man, 66)

Behavioral Response: Changes in Financial Self-Management

They also described how the material burden impacted their financial planning. Some participants decreased day-to-day spending on necessities. As one woman (White, 78) stated simply, “When you get old, you’ve got a choice between medicine and food.” Others decreased participation in leisure activities. One woman (Black, 62) expressed, “I used to be able to do my mani-pedi twice a month. I used to be able to get my hair done every 2 weeks. I would go to the movies once or twice a month. I would go out to eat at least twice a month. All of that has changed.”

Participants sold assets, dipped into retirement funds, or moved residences to pay medical bills. Many expressed that their hopes and expectations for retirement were disrupted by the burden of medical bills. Participants also reported obtaining Medigap or changing Medicare Part D plans to reduce costs. One participant (White, man, 67) included “between $30,000 and $40,000 worth of medical bills” in his bankruptcy filing.

“I sold my house. It's hard. I've been here 20 years. I don't want to move. I thought I'd die in this house. But my health is more important than anything, right?” (Multiracial, man, 64).

“I knew that the day was going to come that I was going to retire... I had gotten everything together so that I could travel. And then this happened... I didn't plan on having to put all my money [into] medicines. And these COPD medications are horribly expensive.” (Black, woman, 75).

“I retired not too long ago, and just a few years prior to that, I bought a boat that I had been dreaming about my whole life. I had to sell it because I had to buy medicine. There was no way I could afford the medication and keep the boat. I've been boating since I was 16 years old. A lot of people go, "It's just a boat." Well, to me, it was the dream of a lifetime and the only nice thing that me and my wife had, so. Now I feel like I’ve gone from living to just hanging around waiting to die.” (White, man, 66)

Participants identified several resources to directly address pharmaceutical expenses such as GoodRx and alternatives to traditional pharmacies, such as Cost Plus Drugs. Some were able to lower pharmaceutical costs through drug manufacturer assistance, while others found their income or insurance made them ineligible. Two participants obtained inhalers from Canada to reduce costs.

“AstraZeneca has a program for Medicare people. When you hit $600 out of pocket, you get it free for the rest of the year. So I don't have to worry about that $115 the rest of the year. But everything else took [my remaining budget]. Insurance took it. House payment took it. So thank God I got that free because I could have never afforded it. And that's one thing I cannot do without.” (White, woman, 78)

Navigating assistance programs presented its own challenges and administrative burdens. Many participants found the application and renewal processes onerous. Others expressed mixed feelings about the constraints of the services themselves.

“I basically lost everything trying to continue to be covered to get treatment for COPD. It took me 2 and a half years.... They just have you running back and forth, running back and forth... In the process of me trying to get disability, I lost my home because I wasn't getting any income at the time to be able to pay my mortgage.” (Black, woman, 65)

A handful of participants were able to access other resources due to comorbid conditions or treatment in subspecialty clinics with dedicated staff. A man with HIV (67) stated, “At the clinic that I go to, I have wraparound services. I have a social worker. I have an insurance specialist.”

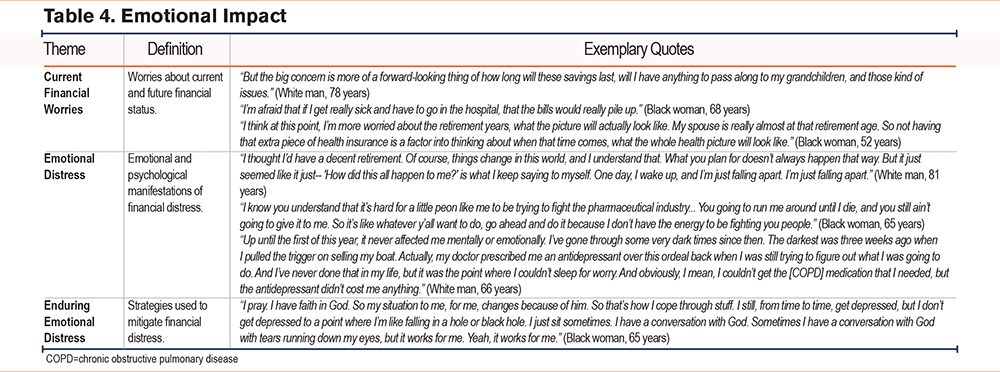

Emotional Impact

Many participants expressed worries about possible future financial problems due to material burden, such as medical bills if their COPD were to worsen, prescription costs, changes in health insurance, and ability to support family members or pass on generational wealth (Table 4). One participant reported being started on antidepressants as a direct result of the worry he experienced from inhaler costs.

“It kind of keeps me on edge. I mean, I have trouble sleeping because at night, when I turn the light out, I'm just a slave to my mind, ‘ Maybe if I did this-- maybe if I did this-- maybe if I hadn't done that .’ So it definitely impacts my well-being and my mental state.” (White, man, 81)

Several participants referenced increased worry in the setting of uncertainty surrounding current and potential government policy changes.

“Cut my Social Security check, won’t be able to survive. They’re talking about taking Social Security away. And if they take away Medicaid, then I won’t be able to get medical help. And even going down to what you’re doing with the research, if we deal with the research, then we won’t progress as far as medically. So yeah, I’m real concerned about that.” (Black, woman, 72)

Participants credited their faith, support systems, and individual qualities such as resourcefulness with helping them endure the emotional impact.

“I just trust in the Lord, and I believe he'll get me through it.” (White, woman, 79)

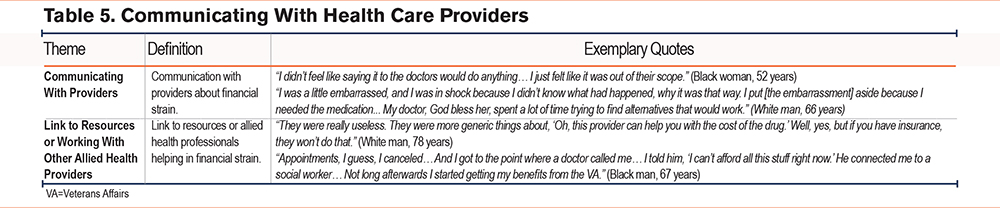

Communicating With Health Care Providers

Participants noted differing comfort levels discussing the material burden of care with providers (Table 5). While some initiated conversations about costs with providers, others expressed the perception that helping in navigating costs was outside of their provider’s scope or interest. Many of those who were connected to allied health professionals, such as social workers or clinic nurses, described ways in which they were able to help the participant navigate assistance programs and administrative burdens. Some who did discuss costs with their providers found their attempts to address costs were inadequate or inapplicable.

“One of the first things that I ask when a doctor prescribes a medicine is, how much is that going to cost? Or in the case of the Dupixent, ‘ I'm sure this is a very expensive drug. ’ But he helped me with writing some letters and navigating the insurance. So that was very helpful.” (White, man, 67)

“I've almost stopped [the Advair] because I just cannot afford it anymore… I've told the doctors about it, and he said, ‘ Well, here's a program you can try to go through. ’ But I never get any satisfaction from them…” (White, man, 81)

Discussion

In this qualitative study of 30 individuals with COPD, we found that financial toxicity impacts many domains of quality of life. Individuals described many contributors to material burden resulting from COPD including high out-of-pocket medical costs, income loss from disability, as well as detractors from long-term financial and credit health such as incurring credit card debt, defaulting on bills, and even filing for bankruptcy. In response to COPD-related material burden, individuals adjusted both their disease and financial self-management. Participants frequently experienced financial worries that impacted their mental health and overall quality of life.

Consistent with prior literature in COPD, the primary driver of direct medical costs in this sample was out-of-pocket costs for inhalers.5,24 Those with Medicare Part D as their sole prescription coverage tended to describe higher out-of-pocket costs, particularly if they had previously entered the Part D “donut hole,” while those covered by Medicaid, Veterans Affairs, or private insurance generally expressed less concern about high copays. In spite of the Inflation Reduction Act’s $2000 cap on out-of-pocket expenses for Medicare Part D beneficiaries starting in January 2025, some beneficiaries interviewed after this provision went into effect who had not previously entered the “donut hole” experienced unexpected increased costs due to higher cost-sharing and deductibles, highlighting the varied impact of this policy.25,26 Insufficient insurance coverage of medication costs frequently led to medication misuse, forgone care, or change in participant regimens. Individual strategies to reduce pharmaceutical costs included seeking pharmaceutical manufacturer assistance, comparing pharmacies for the cheapest prices, and even obtaining inhalers from abroad. Participants described meeting direct medical costs by using savings, selling assets, and incurring debt as well as decreasing spending on both day-to-day necessities and leisure pursuits. Some connected decreases in everyday and leisure spending to increased social isolation and worse quality of life.

To our knowledge, this is the first study exploring experiences of financial toxicity in COPD. Our results indicate that individuals with COPD report similar levels of financial toxicity on the COST-FACIT as seen in cancer.27-29 Many of the themes emerging from our study are consistent with those demonstrated in the oncology literature or after an acute critical illness.30-33 COPD is distinct from these illnesses in that it is a chronic, slowly progressive disease rather than a disease with a sudden, unexpected onset often requiring an upfront intensive diagnostic workup and treatment. Many oncology populations may include younger, working-age individuals who have employer-sponsored health insurance.34-37 Importantly, similar to nationally representative studies of COPD, more than half of our sample were Medicare-eligible adults, reflecting the older average age of people with COPD.38 Lifelong management with chronic inhaled therapies, frequent medication changes, and recurrent exacerbations that may result in emergency department visits or hospitalizations lead to cumulative out-of-pocket costs through premiums, deductibles, copayments, and coverage gaps that persist over many years and often coincide with fixed or limited income in retirement.5,24 As mentioned previously, COPD disproportionately affects people of low SES and is a leading cause of disability, and many individuals may experience work limitation or early exit from the workforce, all of which may result in reduced lifetime earnings and savings.2,39,40 These disease-specific features shape how financial toxicity is experienced and managed by people with COPD.

Considering the interaction between age and chronic disease trajectory, disability, and cumulative costs, participants’ perceived financial toxicity also appeared to be impacted by individual expectations. Many described the discrepancy between their previous postretirement plans and their lived reality, which could be disrupted by progression of disease and the financial impact of changes in insurance coverage, from employer-sponsored to Medicare, at a time in their life when they had limited ability to change their financial situation. More work is needed to understand whether these results generalize to other chronic disease populations.

Our findings have important implications for COPD management. While some individuals described the stress of navigating health care expenses, others who were well-connected to social support systems or eligible for federal or state assistance described minimal financial distress, suggesting that the experience of financial toxicity is not linearly related to income level. These results echo the need for continued federal assistance programs including Medicaid to help individuals manage increased health care costs and access care.41,42 Prior research has shown that patient-centered financial navigation may decrease the burden of cancer-related financial toxicity.43,44 Future research could investigate the impact of financial navigation on individuals with COPD. More immediately, integrating screening for financial toxicity into COPD disease management may help identify individuals who might benefit from additional services.4 Further quantitative research is needed to evaluate the impact of financial toxicity on clinical outcomes such as health-related quality of life, mental health, and health care utilization.

Qualitative semistructured interviews allow for nuanced exploration of participant experiences that may not be adequately reflected by quantitative measures. Nevertheless, our work has several limitations. Although we used purposive sampling to include diverse perspectives, our findings may not generalize to all individuals with COPD since the majority of participants were from one geographic region. Some participants described multiple comorbidities, and in some cases it was challenging to disentangle whether material burden arose from their COPD or comorbidities. Finally, all interviews were conducted by phone, precluding observation of nonverbal cues.

Conclusion

In this qualitative study of individuals with COPD, we found that the material burden of COPD care negatively impacts disease self-management, financial self-management, and psychological well-being. The interaction between older age and chronic disease trajectory, disability, and cumulative costs provides a unique context for experiences of financial toxicity in this population. Future research should focus on the impact of financial toxicity on patient-reported clinical outcomes, such as health-related quality of life, as well as interventions to mitigate financial toxicity.

Acknowledgements

Author contributions: SGM and MNE contributed to the conception and design of the study. SGM conducted the interviews, and SGM and KH conducted data analyses under the supervision of MNE. SGM wrote the initial draft of the manuscript. SGM, KH, CKE, MS, NP, KAR, TJI, and MNE contributed to the interpretation of data and the revision of the manuscript for important intellectual content, approved the final version, and agreed to be accountable for all aspects of the work.

Declaration of Interest

The authors have no financial or other disclosures to report.